Dollar attempts to rally except against Yen

The yen rally continues today on talks that the BoJ may adjust yield curve control again next week. It is also supported by the continued decline in benchmark US and European Treasury yields. Meanwhile, the dollar tries to fight back as US futures dip, reversing some of yesterday’s post-CPI gains. But overall, the greenback remains the second worst performer of the week, behind the Swiss franc and followed by the kiwi. Yen is the best followed by Euro and Aussie.

In Europe, the FTSE is up 0.41% at the time of writing. DAX is flat. CAC is up 0.21%. Germany’s 10-year yield is down -0.017 to 2.107. Previously, the Nikkei was down -1.25% in Asia. The Hong Kong HSI rose 1.04%. China Shanghai SSE rose 1.01%. The Singapore Strait Times rose 0.79%. The 10-year Japanese JGB yield rose 0.0067 to 0.512.

UK GDP grew 0.1% mom in November, avoiding a contraction

UK real GDP grew 0.1% mom in November, much better than expectations for a -0.3% mom contraction. Services grew 0.2% mom. Production fell by -0.2% mom. The construction was flat. Total monthly GDP is -0.3% below pre-pandemic levels.

In the three months to November, GDP fell -0.3% 3mo3mo. There was a -0.1% decline in services, a -1.4% fall in manufacturing with the only 0.3% growth coming from construction.

Also released was that November manufacturing output fell by -0.5% mom, -5.9% yoy versus expectations of -0.2% mom, -5.2% yoy . Industrial production declined -0.2%mom, -5.1%mom, vs expectations of -0.1%mom, -2.8%mom. Goods trade deficit widened to GBP -15.6bn vs. GBP -14.9bn expected

NIESR expects 0.1% UK GDP growth in Q4, Q1 risk on the downside

Following today’s release of UK GDP, NIESR forecasts that December GDP will fall compared to November. Overall, however, service-driven GDP growth of 0.1% is estimated in Q4.

Paula Bejarano Carbo, Associate Economist, NIESR, said: “Given that the purchasing managers’ indices for services, manufacturing and construction are all below the neutral reading of 50 in December, we expect a slight decline in GDP in December compared to November ; That does mean a surge in quarterly GDP, however, possibly a sign that households are enjoying one last hurray before belt-tightening in 2023.

“Looking ahead to Q1 2023, risks to GDP appear to remain on the downside, driven by weak growth in key sectors, weak consumer and business confidence and a widespread fall in real incomes.”

Industrial production in the euro area rose by 1.0% mom in November and by 0.9% mom in the EU

Industrial production in the Eurozone rose 1.0%m/m in November, ahead of expectations of 0.6%m/m. Capital goods increased by 1.0%, intermediate goods by 0.8% and consumer durables by 0.4%, while energy decreased by -0.9% and non-durable consumer goods by -1.3%.

Industrial production in the EU rose by 0.9% month-on-month. Among the Member States for which data are available, the highest monthly increases were recorded in Ireland (+6.4%), Luxembourg (+5.0%) and Malta (+4.6%). The largest decreases were observed in Estonia (-3.7%), Sweden (-3.3%) and Croatia (-1.9%).

Euro-zone exports rose 17.2% yoy in November, while imports rose 20.2% yoy

Euro-zone exports of goods to the world rose 17.2% yoy to €264.7 billion in November. Imports rose 20.2% year-on-year to EUR 276.3 billion. The trade deficit amounted to EUR -11.7 billion. Trade within the euro zone increased by 16.8% year-on-year to EUR 241.5 billion.

Seasonally adjusted, exports increased by 1.0% mom to EUR 251.5 billion. Imports fell -3.8% mom to EUR 266.7 billion. The trade deficit narrowed to -EUR 15.2 billion from -EUR 28.1 billion in October, versus expectations of -EUR 20.0 billion. Euro-zone intraday trade fell to €232.2 billion from €233.4 billion in October.

ECB-Kazakhs: Core inflation is currently an important indicator of inflation persistence

ECB Governing Council member Martins Kazaks pushed back talks that the central bank would cut interest rates by the end of this year. He said he sees no “reasons” for it.

“It would take a deep recession with a sizeable rise in unemployment for inflation to come down, pushing for interest rate cuts,” the governor of the Central Bank of Latvia said. “But that’s not likely given the current macro outlook.”

“It is possible that core inflation will continue to trend higher even if headline inflation is declining, for example due to fluctuations in energy prices,” he said. “In my view, core inflation is currently a key indicator of inflation persistence and policy decisions.”

He expects interest rates to rise “well into restrictive territory” but declined to estimate the final rate. “The uncertainty is too great and we will find it step by step,” he said.

Chinese exports fell -9.9% yoy in December, imports fell -7.5% yoy

Chinese exports plunged -9.9% yoy in USD terms in December, the sharpest drop since February 2020 but slightly better than expectations of -10.0% yoy. Imports fell -7.5% yoy, better than expectations of -9.8% yoy. The trade surplus widened to $78.0 billion from $69.8 billion, slightly above expectations of $77.9 billion.

In CNY terms, exports fell -0.5% yoy while imports rose 2.2% yoy. The trade surplus widened to CNY 550 billion from CNY 494 billion, beating expectations of USD 533 billion.

For 2022 as a whole, exports rose 7.2% in US terms, much worse than the 29.6% in 2021. Imports rose 1.1%, a sharp decline from 30.0% in 2021 .

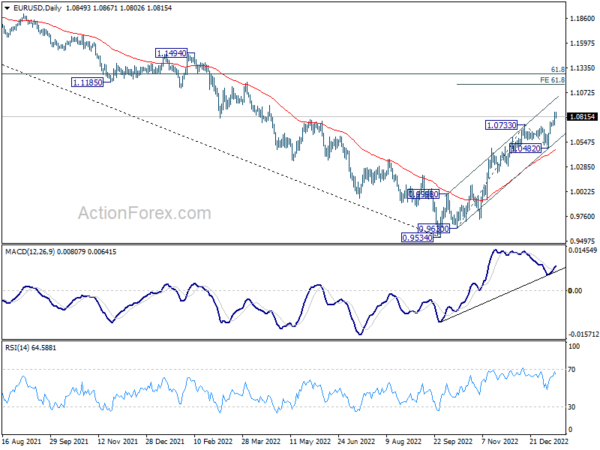

EUR/USD midday outlook

Daily Pivots: (S1) 1.0766; (P) 1.0816; (R1) 1.0902; More…

With 1.0729 minor support intact, EUR/USD intraday bias remains slightly up. Current rise from 0.9534 should target 61.8% forecast from 0.9630 to 1.0733 from 1.0482 at 1.1164 next. On the downside, minor support below 1.0729 will initially neutralize intraday bias again. But near-term outlook remains bullish as long as 1.0482 support holds in case of a pullback.

Overall, recent action suggests that the rally off the 0.9534 low is more of a medium-term uptrend than a correction. Another rally calls for a 61.8% retracement from 1.2348 (2021 high) to 0.9534 at 1.1273 next. This will remain the preferred case as long as 1.0482 support holds

Update of economic indicators

| Greenwich Mean Time | Ccy | events | Indeed | forecast | previous | Revised |

|---|---|---|---|---|---|---|

| 11:50 p.m | JPY | Money supply M2+CD Y/Y Dec | 2.90% | 3.30% | 3.10% | |

| 03:20 | CNY | Trade Balance (USD) Dec | 78.0B | 77.9B | 69.8B | |

| 03:20 | CNY | Exports (USD) Y/Y Dec | -9.90% | -10% | -8.70% | |

| 03:20 | CNY | Imports (USD) y/y Dec | -7.50% | -9.80% | -10.60% | |

| 03:20 | CNY | Trade Balance (CNY) Dec | 550B | 533B | 494B | |

| 03:20 | CNY | Exports (CNY) Y/Y Dec | -0.50% | 0.90% | ||

| 03:20 | CNY | Imports (CNY) Y/Y Dec | 2.20% | -1.10% | ||

| 07:00 | British pound | GDP M/M Nov | 0.10% | -0.30% | 0.50% | |

| 07:00 | British pound | Directory of Services 3M/3M Nov | -0.10% | -0.40% | -0.10% | |

| 07:00 | British pound | Manufacturing Production M/M Nov | -0.50% | -0.20% | 0.70% | |

| 07:00 | British pound | Manufacturing Production Y/Y Nov | -5.90% | -5.20% | -4.60% | -5.70% |

| 07:00 | British pound | Industrial Production M/M Nov | -0.20% | -0.10% | 0.00% | -0.10% |

| 07:00 | British pound | Industrial Production Y/Y Nov | -5.10% | -2.80% | -2.40% | -4.70% |

| 07:00 | British pound | Goods Trade Balance (GBP) Nov | -15.6B | -14.9B | -14.5B | -12.3B |

| 09:00 | EUR | Italy Industrial Production M/M Nov | -0.30% | 0.40% | -1.00% | |

| 10:00 a.m | EUR | Eurozone trade balance (EUR) Nov | -15.2B | -20.0B | -28.3B | -28.1B |

| 10:00 a.m | EUR | Eurozone Industrial Production M/M Nov | 1.00% | 0.60% | -2.00% | -1.90% |

| 12:00 p.m | British pound | NIESR GDP estimate (3 months) Dec | 0.10% | -0.30% | ||

| 1:30 p.m | USD | Import Price Index M/M Dec | 0.40% | -0.90% | -0.60% | |

| 15:00 | USD | Michigan Consumer Sentiment Index Jan P | 61.6 | 59.7 |