How can banks integrate climate risks?

This year, too, the central theme is World Economic Forum from davoswhich opens today will be the one climate change. After Intergovernmental Panel on Climate Change (IPCC) of the United Nations, indeed one is needed Reduction of greenhouse gas emissions by 43% by 2030 to achieve the climate goals of the Paris Agreement. But the IPCC itself assesses that Emissions will increase again by almost 11%.

Also according to the report Global climate highlights 2022 from Copernicusthe earth observation program of the European Union temperature The world average in 2022 was 1.2 degrees higher than in the pre-industrial era (1850-1900). The summer of last year broke the heat record in Europe that was set in the summer of 2021. Autumn 2022 was the third warmest on record in Europe. Climate change affects the functioning of the economy due to the action of two types of climate risk:

- physical risks related to climate change, including increased frequency or severity of weather phenomena such as storms and droughts;

- transition risks from a traditional economy to a carbon neutral one.

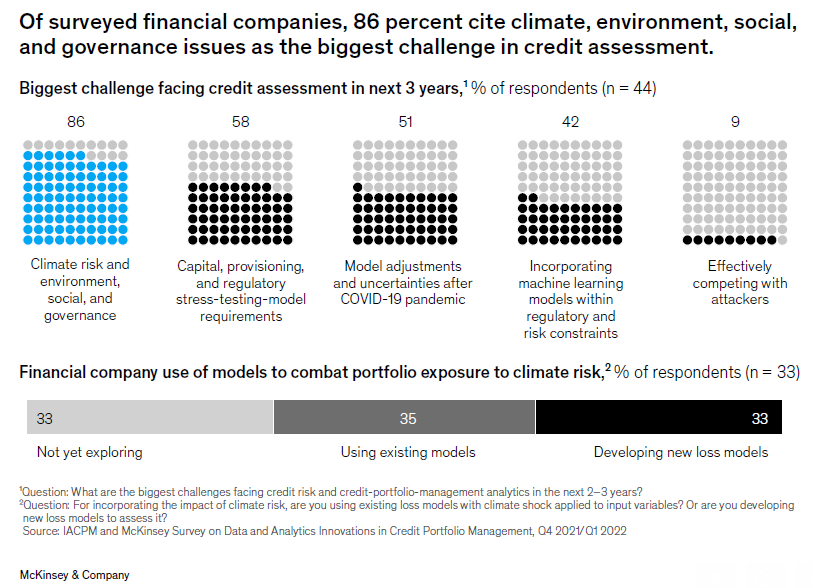

The analysis “Data and analytics innovations in credit portfolio management”edited by McKinsey & Co and fromInternational Association of Credit Portfolio Managers (IACPM), which is based on interviews with 44 financial institutions worldwide, has taken stock of the key impacts of climate risk on lending. Let’s see what they are.

The impact of climate risk

Climate risk is typical focused on specific areas. It has been determined that physical risk and transition risk exist in very specific areas of the portfolio. To identify areas of high concentration of climate risk impacts, financial institutions need to conduct detailed mapping to focus their efforts on priority risks for each of the high-risk portfolios. For example, it is commonly observed that the bulk of the credit impact (approximately 70-80% of the incremental impact) for real estate-related asset classes comes from the 10-20% of obligors in the portfolio.

The average impact on creditworthiness may be modest in the short term, but there will likely be one high variability at the level of the individual debtors. The analysis shows that even in sectors exposed to high physical and transition risk, the aggregate/average impact on the portfolio can be moderate. For example, in a portfolio of upstream oil and gas companies, the average impact might be an EBITDA reduction of about 7%. However, the difference between high and low impact borrowers can be significant. In the Oil & Gas upstream portfolio just mentioned, there are several companies that negatively impact Ebitda by up to 40%, while others have a positive impact on Ebitda in some scenarios through the redistribution of oil and gas demand. Financial institutions have started to assess these impacts and intend to study them further, suggesting there is still a long way to go.

In industries exposed to physical risk, most of the risk is represented by chain effectsnot from direct damage. The short-term credit impact of direct losses is typically covered by insurance in industries such as real estate (both commercial and retail). However, the knock-on effects may outweigh the direct effects, and any assessment of significant risk factors should include paying higher insurance premiums and worsening a community’s standard of living, while the property itself may not be harmed.

Uncontrolled climate risk can a noticeable impact on returns and economic gains. The Comprehensive Capital Analysis and Review (CCAR), the stress tests imposed by European Central Bank o Methods based on regulatory capital may not be appropriate for assessing climate risk, note McKinsey & Company and the International Association of Credit Portfolio Managers (IACPM). In fact, these methods focus on capital risk and may underestimate the credit impact on individual borrowers. Assessing climate risk requires an understanding of returns on climate-related new assets and specific scenario analysis for individual borrowers. If not done optimally, the impact can be significant. In the case of a North American bank, they estimate apotential erosion of 35% of profits by 2030 in the absence of interventions in the main areas of exposure to climate risks.

Obstacles to climate risk assessment

Before addressing and mitigating climate risks, financial institutions need to address it multiple hurdles in terms of skills, data, and analytics. As many of the existing risk assessment tools were not developed based on climate assessment requirements, financial institutions need an open architecture that supports new methods for quality, standardization and data collection. Ultimately, more focus needs to be placed on capturing and addressing the holistic impact of climate risk on the portfolio interdisciplinary skills and on the transversal mobilization of credit managementof front line and gods risk models.

Financial institutions in particular must comply with this significant advances in two key approaches to climate risk assessment: Climate scenario analyzes and the integration of climate into credit processes. As institutions build climate risk assessment capabilities through risk identification and analysis of climate scenarios, the next step is to develop a credit decision-making approach that ensures that climate risks are appropriately and sufficiently considered in portfolio construction and management. In order to achieve this, it is necessary Integrate quantitative climate risk analysis into the credit assessment process.

Banks and climate risk analysis

To date, the banks that started the climatic stress tests they are considering developing new credit models or adapting existing ones to stress tests. Respondents from McKinsey and IACPM split evenly into three parties and indicated that they are developing new models to estimate expected losses, are using current models, or are new to the topic. Additionally, analyzes of loss scenarios due to climate stress were more focused on mid-market, corporate and commercial real estate portfolios (more than 50% of banks for each segment), while a smaller number of banks (less than 40%) performed these analyzes on SME portfolios. Most financial institutions in Europe, the Middle East and Africa are developing models internal or rely on it Third-party climate risk assessment models. Institutions from Asia-Pacific are the least advanced, and those from North America fall somewhere in between. It is no coincidence that 86% of respondents consider climate risks andIT G as the next big challenge for credit risk analysis and portfolio management in the next two to three years.

Banks and climate risk